Grace Technology - Did you read the instructions?

Digital Talent

Grace Technology (6541) | Quick Look

Share Price ¥2,677 | Mkt Cap $800m

Does anyone read instruction books anymore? Last week, while out in the car, one of those annoying dashboard warning lights started to blink.

Obviously, rather than just call the AA, I decided to consult the owner’s manual – all 500 pages of it - Urgh. Of course, I eventually gave up and called for roadside assistance. But it was a fun wait.

Leafing through the manual, on page 35, I was reminded “Do not dispose of the vehicle yourself.” Duh. On page 50, “Never use a cup holder to hold hot liquids while the vehicle is moving.” Ouch. Here’s something that I had done before on page 70, “Do not fold down the rear seats when occupants are in the rear seat area.” Oops, sorry kids.

It turned out there was nothing wrong with the car, but there was plenty wrong with the instruction manual. I mention this to illustrate how important instruction manuals are and how one company in Japan is creating an incredible business out of this arcane area.

What does Grace Technology do?

In simple terms, Grace produces product manuals for the manufacturing industry. Every time Tokyo Electron, for example, ships a new etching machine, it comes with the following: Introduction manual, operating manual, programming manual, tutorials, maintenance manuals, and parts manuals. The increasing complexity of the products and services drives the volume of manuals. That’s a great business.

The company splits its revenue into two lines:

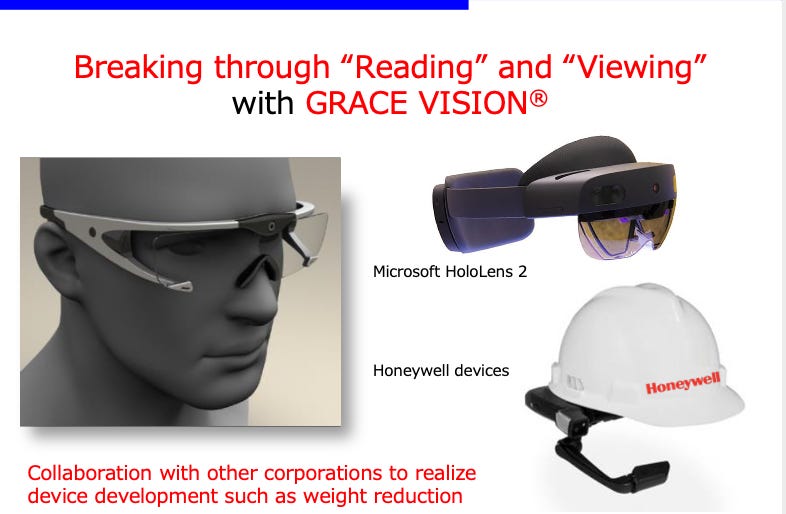

1) Manual Management System (MMS) - planning, development, operation and management of “e-manuals” via a cloud service dedicated to manual production and management. GRACE VISION – a next generation AI manual business, with Augmented Reality glasses, will be a part of this segment, once it kicks off.

2) Manual Order-Made Service (MoS) - the writing and translation services focused on technical products for the manufacturing industry. The recently consolidated acquisition, Hotaru, became part of MoS in the last quarter, which is why sales suddenly jumped.

What are the key sales drivers?

Digital Transformation. It may be a buzzword, but it is hard not to appreciate how reliant Japan had become on paper. Just as many other paper processes have shifted over to the cloud, the manual creation process is ripe for innovation. Grace is at the forefront of that shift.

Money. Outsourcing manual production can save money for the client company. Lots of money. Currently, in-house engineers are tasked with writing manuals. However, there are different people writing for each product, it is time consuming, and fails to achieve any consistency. This results in errors and inconsistencies between manuals, mistranslation to foreign languages, and in a worst case, production delays. The result is frequent inquiries and complaints from customers.

Is it an attractive market?

I must say, this surprised me. Grace tells us that the potential market size for manuals in Japan is around $60b.

According to some studies, Japanese manufacturers spend around 1% of sales on manual production, the majority of which must be done in-house. Looking at MOF stats, Japan’s manufacturers sold an impressive $3,600b of goods in 2020. That would imply a $36b spend on manuals. Remember, that is just manufactured goods, so Grace’s number (including services) could be about right. That is an impressive runway for growth in anyone’s book.

Given that Grace has $21m in trailing 12M revenue, it is quite easy to imagine that this market is highly fragmented and ripe for consolidation. There are over 2,500 translation companies and 100 production companies involved in the industry. It is also ripe for outsourcing. If Grace can save clients around 25% on manual production costs, that would create $9b of value for the manufacturing sector alone. Just to put that into perspective, the market cap of Yamaha Motors is $9b – it is a big number.

Is Grace a winner?

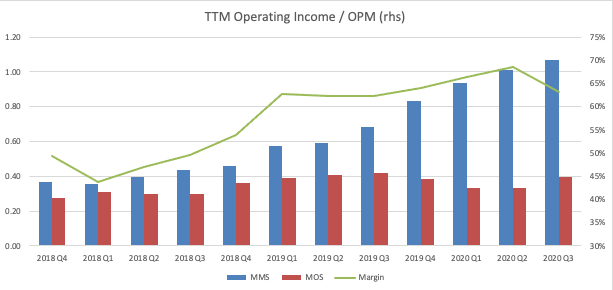

The quick answer is yes. Over the past eight quarters, Grace has achieved an average operating margin of 50%. That leads me to believe that Grace has the following competitive advantages on its side:

Cost Advantage – Grace has promoted the modularization and standardization of product manuals for the manufacturing industry. Even the labour intensive MoS business has been turned into an efficient artform. Grace carriers out the high-value added consulting steps and then farms out the low value-added technical writing, DTP and translation. They have created a unique “people light” workflow.

Switching costs - The cost advantage is amplified even further in the MMS business. The use of technology and the cloud provides clients with a tool for manual planning, production and management, reducing costs even further. Grace currently offers the e-manual service to 62 clients, up from 44 a year ago. Grace charges initial consulting fees and a monthly usage fee for this service. As with most software in the cloud, e-manual gives Grace pricing power by locking in customers to its unique ecosystem.

Is it a good stock to own?

All small cap growth stocks in Japan are pricey. Grace is no exception. On management’s guidance for the year to March 2021 (results should be released soon), the stock is trading at an EV/Rev of 35x. That is up there with the very best SaaS business models.

However, given the huge addressable market and strong competitive position within the industry, it is hard to imagine that this company will not have materially higher revenues over the next five years.

We haven’t even touched yet on the potential for the new Grace Vision product - the company has a Japanese patent and US patent pending for this revolutionary product that brings manuals to life: complete guidance with audio, lighting and arrows. The AI assistance can help with the remote monitoring and support of equipment. The eventual goal is to list this company on Nasdaq.

In short, there are a number of reasons why we like this stock and are happy long-term investors.

Help Wanted - Digital Talent

Great news from Kasumigaseki this week - the Lower House passed the bill to establish the Digital Agency. The Agency will revitalize Japan’s inefficient and creaking public sector systems, leading to a more modern, efficient and effective government. There will be knock-on benefits - where the government goes, so too does the private sector and society at large. Great! Not to be bad news bears, but we do wonder where the new Digital Agency is going to find the required 500 IT engineers. Will $100k/pa be enough to lure talent from the private sector? The Digital Agency is a fantastic idea, but Minister Takuya Hirai needs to see the big picture.

Japan lacks software engineers – it is a well-known issue that keeps cropping up. A recent McKinsey report highlights that software engineers make up just 1% of the Japanese workforce. Furthermore, this talent is concentrated in the large systems integrators – the likes of Fujitsu and NEC. Exacerbating the supply issue, only 1% of undergraduate students in Japan are studying computer science-related courses versus 4% in the United States. And that's just the supply side.

It’s just as bad on the demand side. To remain competitive, technology firms continue to bid up tech talent. Z-Holdings, for example, announced it intends to employ 5,000 AI/IT engineers to boost its platform. And that’s the issue. METI estimates that the economy is short of 170,000 digital workers, with the number forecast to reach 430,000 by 2025. This doesn't bode well for the Digital Agency's staffing target. Big companies will be willing to pay multiples of what the government can offer. Where will the government’s 500 hires come from? Startups? Unlikely. The pay may be lower, but talented IT engineers who go to startups are there because of something else - they are following their dreams. A desk job in a government agency is hardly likely to appeal. So, where does this leave us?

Clarity on the scale of the HR challenge is needed. The decision-makers need to attack the problem on at least two fronts. Firstly, Minister Hirai needs to offer genuinely competitive salaries and incentives to get the best talent in the door. The second part involves supply. Just 1% of students taking computing courses at universities does not cut it. Computer science courses, both online and offline, must be expanded and incentives provided to attract more students. We are living in the digital age and Japan faces a demographic time bomb that makes digital transformation a must. Getting the Digital Agency up and running is Hirai’s first challenge, but the bigger picture is arguably more important.

🗞 NUGGETS 🗞

SPIDEY SENSES. Sony has signed a $1b deal with NETFLIX to stream the studio’s films after their theatrical release (starting in 2022). This is disruptive for other studios that compete with Netflix in streaming. LA Times

GENETIC LEAP. Softbank will invest nearly $1.2B into genetic-testing provider Invitae (NVTA US). SoftBank is beefing up its portfolio of biotech and life-science companies....presumably to bring pepper to life. WSJ

DIGITAL YEN. Kuroda is a 💎🙌 $hodler...almost. The BoJ joins every other central bank in trying to figure out what to do with its printing presses. Reuters

CASH(IER) LESS. Aeon will open stores in Tokyo that have no cashiers: cameras and sensors will identify customers and automatically charge the cost of the purchase. Aeon’s learnt these new tricks from its stores in China and its tech partner, Cloudpick. Nikkei

CVC SHOPPING. Foreign Private Equity firm, CVC, launched a $20b bid for Toshiba. There are a lot of hurdles to overcome. First, CVC would need to clear Foreign Exchange and Foreign Trade Act due to Toshiba’s national security status. Secondly, Toshiba is well held by activist investors that may want considerably more for their shares. CEO Kurumatani would just love to get the activist investors off his back, but this is going to be a tough deal.

📈 MOVERS and SHAKERS 📈

This week, small cap growth did well, with over 55% of the 140 stocks in our Japan Innovation & Disruption (JID) universe up on the week. The TSE Mothers Index rose +1.6%.

🔺+25% WealthNavi (7432, Mkt Cap $1.9b), provider of fully automated robotic advisory services, reported that its AUM now tops over ¥400b ($3.7b).

🔺+22% Kaizen Platform (4170, Mkt Cap $320m), a company that helps firms go digital, rallied in celebration of the government passing the Digital Agency bill.

Have a great weekend! We would be delighted if you could share this newsletter with your friends. 🙏